LO 23.1: Demonstrate knowledge of the five beneficial characteristics of allocations to commodity futures

• List the five beneficial characteristics for investors when allocating to commodity futures. • Describe the effects of full collateralization on commodity risk, diversifying a traditional portfolio with commodity futures, and adding commodities exposure in an asset-liability management investment setting. • Describe the hedging benefits of commodity futures over time and in various economic cycles. • Discuss the performance of commodities in each of the four major business cycle phases. • Explain how mean reversion can be a great benefit of commodity investment. • Understand why commodity investment may be well suited to capture diversification return. • Explain why volatility reduction enhances geometric mean returns, but does not enhance expected values in commodity investing. • Discuss the source of positive risk premium of commodity investments and the effect of this positive risk premium on investment decisions. • Discuss the source of positive skewness of commodity investments and the effect of this positive skewness on investment decisions.

Five beneficial characteristics of allocations to Commodity Futures

• Ability to hedge inflation, business cycle, and event risk. • Improved risk and return profiles of portfolios due to commodity futures’ low correlation with stocks and bonds. • Improved performance through rebalancing a portfolio called the diversification return due to commodity prices exhibiting mean reversion. • Potential for a positive risk premium and roll return. • Positively skewed return distributions.

Diversification benefits of Commodities Futures

- Greater than with spot market; captures the convenience yield. - Better than owning stocks of commodity-based firms for diversification purposes. - Superior div’n and liquidity benefits relative to other alts such as real estate. - Correlation between comm and equities&bonds are negative, become more negative around the 5 year time horizon. - Studies indicate that over time, correlation between S&P GSCI and Global stocks is increasing, making div’n benefits decrease over time.

FINANCIALIZATION OF COMMODITY MARKETS

- resulte of money flowing into commodities, becoming more more integrated into theinvestment universe. Increases correlation to the financial markets.

Commodities Futures as an inflation hedge

Inflation rate is positively correlated to an equally wieghted portfolio of commodity futures prices at all time horizons, even more so for longer horizons. - vs. stocks which is negatively correlated to inflation in long term, and bonds which is negatively correlated in short term. - Comm Indices are very useful for heding inflation - individual comm’s vary in usefulness for this. -Precious Metals, Industrial metals, and energy products can be good inflation hedges

Business Cycle Diversification

- Works different than STocks throughout the business cycle, provide good diversification against systematic risk

event risk

exposure to signficant events that have potential to cause large negative returns for stocks. - commodities generally have positive exposure to events , creating low or negative correlation with traditional assets. (tend to benefit from unexpected events). -

Mean reversion

the tendency for an asset’s price to return to its long running average value. Commodities have this. -

DIVERSIFICATION RETURN

Effect of Rebalancing a portfolio of commodities that exhibit mean reversion back to its original target asset allocation will result in an increased average or geometric mean return. Result of two factors: 1) Reducing the allocation to assets that have increased in value back to their target weight capturing their positive returns. When they mean revert, the impact of their negative returns on the portfolio will be lessened due to their reduced weight in the portfolio. 2) Increasing the allocation to assets that have decreased in value back to their target weight resulting in an increased return to the portfolio when they mean revert and increase in value.

What two properties allow Commodities to have Diversification Return

(1) low correlation between volatile assets in a portfolio, and (2) individual asset prices exhibit mean reversion.

Commodity Skewness and Kurtosis

- Commodities have positive exposure to less predictable events, which positively skews their return distribution. It is not present in all time periods however. - Commodities are associated with higher kurtosis (Fat tails) than trad investments.

LO 23.2: Demonstrate knowledge of commodity investment strategies.

• Discuss the unique risk and return characteristics of commodities, as compared to traditional investments.

LO 23.3: Demonstrate knowledge of directional strategies.

• Describe directional strategies in commodities markets

DIRECTIONAL COMMODITY sTRATEGIES

Based on a forecast of the direction of the market, and are exposed to systematic risk - generally establish long or short positions in commodity derivatives (listed futures, options, OTC forwards and swaps) based on forecasts of comm price changes. - 2 groups - Fundamental Directional Strategies, and Quantitative Directional Strategies

Fundamental directional strategies (1 of 2 Directional Commodities Strategies)

- use supply and demand analysis as well as fundamental macro factor analysis (interest rates, econ growth, currencies, industry factors) to determine the direction of commodity Prices

Quantitative Directional Strategies (2 of 2 Directional Commodities Strategies)

- identify undervalued or overvalued commodities using technical and quant indications (moving average systems) - often focus on roll yield, conveninece yield, and risk premium

LO 23.4: Demonstrate knowledge of relative value strategies

• Describe relative strategies in commodities market

Relative value strategies

based on identifying mispriced assets and hedging their market exposure - use sector-specific expertise of fund manager to trade the relative price difference betwen commodities based on one or more risk dimensions. Three of the risk dimensions: 1. Location. A single commodity can have different prices in different markets. 2. Correlation. Two commodities may diverge from their historical price correlation. 3. Time. A single commodity can have different prices for different delivery times.

LO 23.5: Demonstrate knowledge of commodity futures and options spreads.

• Describe various types of calendar spreads, and calculate the position profit and loss for a commodity spread trade. • Describe processing spreads, including typical users and common types. • Describe substitution commodity spreads, two major types of substitutions in commodities, and how to determine entry and exit points with a substitution test statistic. • Describe quality and location spreads, and how they differ from substitution spreads. • Describe intermarket relative value strategies

Commodity spread strategies

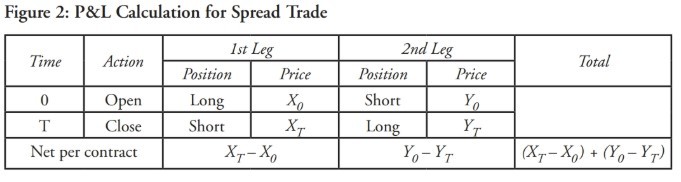

- refer to trading strategies that capitalize on the relative mispricing of two or more commodity-related invesstments. - Sub-strategies include calendar spreads, processing spreads, substitution spreads, quality spreads, location spreads, and intramarket relative value. - For a commodity spread trade, two positions are opened at the same time and later closed at the same time. Thus, there are four transactions in total.

P&L Calculation for Spread Trade (Table for reference)

Commodity Time Spreads

exploit trading opportunities among commodity derivatives including futures, forwards, swaps, and options across the time dimension.

Calendar Spread

- Most basic time spread, involves taking long and short futures positions for different delivery times and can be customized to provide liquidity or insurance

- Liquidity trade - eg taking a long position in a futures contract for delivery in a specific month, taking a short position in a futures contract with a slightly longer maturity. Trade absorbes excess short contracts in the market (provides liquidity) through the shorter term contract, offsets the position through the longer contract with expectation that prices will rise, and generate a profit

- Insraunce trade - eg taking a short position in March natural gas futures contracts and offseeting long position in April contracts will be profitable in a mild winter (warm weather will push the price for March delivery below the trader’s contract selling price, generating a profit) - could suffer signficant losses if harsh winter though.

- This is related to selling a synthetic weather derivative (i.e., insurance against a harsh winter)

- Insraunce trade - eg taking a short position in March natural gas futures contracts and offseeting long position in April contracts will be profitable in a mild winter (warm weather will push the price for March delivery below the trader’s contract selling price, generating a profit) - could suffer signficant losses if harsh winter though.

Calendar Spreads (Bull vs Bear)

- bull spread - this takes long futures positions in a short term contract and short position in longer term contract - in contangoed [vs. backwardated] markets, the trade is profitable if the spread between the contracts narrows [vs. widens]. Losses on bull spread trades are limited to the cost of carry (adjusted for convenience yield) assuming the market is efficient and no arbitrage opportunities are available.

- Bear spread. This strategy takes a short futures position in a short-term contract and a long position in a longer-term contract. In contangoed (backwardated) markets, the trade is profitable if the spread between the contracts widens (narrows). Losses on bear spread trades are potentially unlimited because the short-term contract can theoretically rise infinitely.

-

1 / 1 - Professional Standards and Ethics8

-

5.1/14 Real Estate as an Investment19

-

5.2/15 Real Estate Indices and Unsmoothing Techniques54

-

5.3/16 Investment Styles, Portfolio Allocation, and Real Estate Derivatives28

-

5.4 / 17 - Listed Versus Unlisted Real Estate Investments32

-

5.5 / 18 - International Real Estate Investments25

-

5.6 / 19 - Infrastructure as an Investment49

-

5.7 / 20 - Farmland and Timber Investments24

-

5.8 / 21 - Investing in Intellectual Property30

-

6.1 / 22 - Key Concepts in Commodity Markets45

-

6.2 / 23 - Allocation to Commodities36

-

6.3 / 24 Accessing Commodity Investment Products44

-

7.1 / 25 - Managed Futures36

-

HALF DONE 7.2 / 26 - Investing in CTAs22

-

NONE YET 7.3 / 27 - Relative Value Strategies0

-

7.4 / 28 - Hedge Funds: Directional Strategies51

-

JUST STARTED 7.5 / 29 - Hedge Funds: Credit Strategies11