Acquisition Costs

Acquisition costs, which are capitalized as part of the cost of the asset, include not only the purchase price of the asset, but also costs associated with obtaining it and preparing the asset for its intended use.

- Include all costs of acquisition or construction as well as preparation for use.

- Purchase price

- Legal fees

- Delinquent taxes

- Title Insurance

- Transportation (freight-in)

- Installation

- Test Runds

- Sales Taxes

- The cost of land includes:

- purchase price (including any existing building that is to be demolished)

- surveying

- clearing, grading, and landscaping

- costs of razing or demolishing an old building are added to the land cost

- proceeds from the sale of any scrap (old bricks) are subtracted from the land cost.

Lump Sum Purchases

If the land and building are purchased for a lump sum, use the Relative Fair Value method to allocate the value between both assets.

- If land/building purchased for $600,000 and the only info available is the tax appraisal of $100,000 to the land and $400,000 to building then use the proprotionate of tax amount to allocate purchase price. (i.e 100/500 or 20% for Land and 400/500 or 80% for building.

- For oil and gas properties, the cost of property includes cost of acquisition and preparation of the property for drilling, as well as any estimated restoraction cost for the property following the completion of drilling (ARO).

Asset Retirement Obligation (ARO)

- Liability recorded at FMV for expected restoration costs expected to be paid at the end of period of usage.

- If not able to determine then should use the PV of the expected future costs.

- The liabliity will have to be increased each year based on the discount and reported as accreation expense (a form of interest expense)

- considered long-term and is amoritzed using the effective interest method.

Disclosures:

- Description of the obligation and related asset

- Description of how fair value was determined

- The funding policy

- A reconciliation of the beginning and ending carrying value

Capitalization of Interest

- Interest cost incurred during the construction period needs to be capitalized. The amount capitalized is considered the avoidable interest (could have avoided had you not built the building). This amount is added to the cost of building the asset.

- Capitalize interest cost if asset is:

- Constructed for company’s own use (built by self or oursider)

- Assets manufactured for resale resulting from a special order (ships)

- Do not capitalize interest if:

- Costs are incurred after completetion of construction

- inventory manufactured in the ordinary course of business

- Amount to be capitalized is:

- Weighted average accumulated expenditues x interest rate = capitalized portion of interest.

- Interest on other debt that could have been avoided by repayment of debt

- Never exceed actual interest cost

- Capitalize interest cost if asset is:

Costs incurred After Acquisition

- Repairs and maintenance expense - costs incureed to keepor restore an asset to its nomral operating condition. These costs are expensed as incurred.

- If the cost makes the asset BIGGER, BETTER, or LONGER that’s GOOD, since one would rather capitalize the cost than expense it.

- Bigger or Better

- Asset X

- Cash X

- Longer (subtract from accum depre to increase carrying value)

- Accum Dep X

- Cash X

- Bigger or Better

- Refurbishment - replace part of the asset

- Identifiable- account as if sold old part and replacing with new part

- Acc Dep X

- Loss X

- Asset X

- Asset X

- Cash X

- Not Identifiable

- Enhances the asset

- Asset X

- Cash X

- Asset X

- Increases the assets useful life

- Acc Dep X

- Cash X

- Acc Dep X

- Enhances the asset

- Identifiable- account as if sold old part and replacing with new part

Depreciation Methods

- Straight Line Method

- Sum of the Years Digit

- Double Declining Balance

- Units of Production

Straight Line Method

- Used when assest give equal benefits to the company throughout their useful lives (example a building)

- depreciation expense is the same amount each year

- depreciation rate = 1/useful life

- (Cost - Salvage Value) / Useful Life

- considers depreciation as a function of time instead of a function of usage

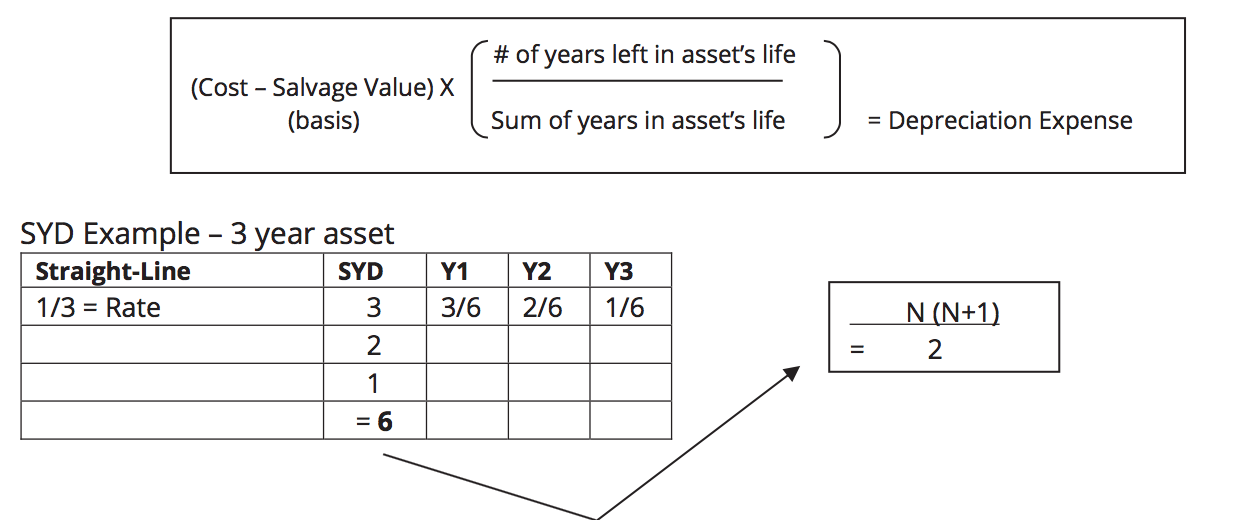

Sum of Years Digits

- an accelerated depreciation method that is considered less aggressive than the double declining method.

- numerator = the number of years left in the asset’s useful life. For example, if it was a 3-year asset then in the first year would be 3, then 2, then 1.

- denominator = the sum of the years in the assets useful life N (N+1)

2

Double Declining Balance

- a depreciation rate that is twice the straight-line rate is applied against the book value of the asset.

- Salvage Value is ignored

- Depreciation expense should not be reduced below the salvage value. In the final year either:

- calculate depreciation expense in the last year as the amount to reduce the carrying value to the salvage value.

- switch from DDB to either SYD or S/L toward the end of the asset’s useful life, depreciating the asset to its Salvage value.

- Balance declines, rate stays the same

- Never get to zero, so eventually must switch over to another method.

Accelerated Depreciation Expense Benefits

- Assumes depreciation is a functionof use (machine hours) or productivity (finished widgets) instead of the passage of time.

- Benefits of accelerated methods

- Better matching since asset is more productive in earlier years

- Minimize loss due to obsolescence. Since the asset was depreciated more quickly, the Carrying value is lower therefore the loss is smaller.

- Helps to even out expenses. Since Repairs and Maintenance in the earlier years is lower, if we take more depreciation earlier on, the total expenses would be more constant over time.

Units of Production (UOP) - Activity Method

- Assumes depreciation is a function of use (machine hours) or productivity (finished widgets) instead of the passage of time.

- Depreciation Expense:

(Cost - Salvage Value ) X (Hours this year/Total Est Hours)

Group or Composite

- Depreciate as a group (e.g. a fleet of trucks)

- Group refers to a collection of assets that are similiar in nature and have approx same useful life.

- Composite refers to a collection of assets that are dissimilar in nature and have different lives.

- Problems occurs when you sell one of the assets in the group. Accum. depreciation is not known.

- assume cash received = carrying value

- assume no gain/loss

- Plug Accum Deprec

Cash 20

Acc Depre 80 (Plugged)

Loss 0

Asset 100

Gain 0

Appraisal or Inventory Method of Depreciation

This method is rarely used. Under this approach, an estimate is made at the end of each year of the value of the assets, and sufficient depreciation expense is recorded to reduce the CV to that amount. Since this approach doesn’t systematically match costs to benefits, it is only used when the loss in value is directly related to productivity, such as for property being rented to others.

Depletion

When assets like PP&E have limited useful lives, some assets actually get used up. Mining companies and others in what are referred to as extractive industries will buy or otherwise obtain rights to real property that is expected to have some natural resource, such as oil, minerals, precious metals, or other commodities.

When property with a natural resources is acquired, the cost is allocated to the property and the natural resource based on their relative estimated fair values. As the natural resource is extracted from the property, the cost is transferred from the natural resource to inventory and ultimately to cost of sales when the inventory is disposed of.

Three step method:

- The total volume of the resource is estimated

- Total volum is divided into the remaining cost, referred to as the depletion base

- The amt per unit is multiplied by the amount extracted during the period to determine the depletion for the period

Depletion = (Depletion Base / Total Vol at Beg of Year) X Units Extracted

Impairments Examples

Examples of impairments include:

- a significant decrease in market value of asset

- significant change in assets physical condition or manner in which it’s used

- signifcant advese change inlegal facors or in the business climate that affects the value of the asset

- accumulation of costs signifcantly in excess of the amount originally expectd to acquire or construct the access

- projection or forecast that demonstrates continuing losses associated with an asset.

- an expectation that is more likely than not that the asset will be disposed of before the end of its expected useful life

Disposal of Fixed Assets

When a company disposes of a fixed asset, they will normally remove the original cost and accumulated depreciation, record any amounts received or due to them as a result of disposal, and recognize a gain/loss for the difference. The gain/loss is reported in continuing operations as part of other items.

Cash 2,500

Loss On Sale 500

Accum Depreciation 7,000

Machinery & Equipment 10,000

Nonmonetary Exchanges

Nonmonetary exchanges are generally recognized at fair value:

- the sales price of the asset surrendered is considered its fair value:

- if the fair value of the asset given is not readily determinable, the assumed sales price will be the fair value of the asset received plus any monetary consideration received or minus any monetary consideration given

- if neither fair value is readily determinable, the assumed sales price will be the carrying value of the asset surrendered.

- A gain or loss on disposal, equal to the difference between the sales price and carrying value of the asset, will be recognized in income

- the asset acquired will be recognized at the sales price amount minus any monetary consideration received or plus any monetary consideraton given

There are 3 circumstances in which a nonmonetary transaction has an assumed sales price that is equal to the carrying value of the asset given, with no gain or loss recognized:

- Transactions in which neither the fair value of the asset given nor the fair value of the asset received can be readily determined

- transactions that lack commercial substance

- an exchange of assets sold in the ordinary course of business for assets sold in the same line of business (inventory for inventory) to facilitate sales to 3rd party customers.

Process to determing Impairment Loss

- Review events or changes in circumstances for possible impariment, if none are identified, no further testing is required.

- if the review indicates impariment, apply the recoverability test. If the sum of the expected future net cash flows from the long-lived asset is less than the carrying amount of the asset, an impairment has occured.

- The impairment loss is the amount by which the carrying amount of the asset is greater than the fair value of the asset. The fair value is the market value or the present value.

Disclosures related to Impairment

- Description of impaired assets and circumstances which led to impairment

- amount of impairment and manner in which fair value was determined

- Caption in income statment in which impairment loss is aggregated, if it is not presented seperately

NOTE that estimated future cash flows are used to detmine if impairment has occured but the asset is adjusted to its estimated fair value, not estimated future cash flows, once the determination has been made.

Impairment of Long Lived Assets to be Disposed of

(Held for Sale)

- Reclassified from PP&E to Other Assets

- when first transferred to held-for-sale category, the amount is the lower of asset’s carrying value and its NRV, which is its estimated selling price less costs of disposal

- assets held for sale are not depreciated

- in subsequent periods, increases or decreases in the NRV are recognized:

- the asset is increased/decreased to its NRV at the B/S date, provided it is not increased to an amount that exceeds its CV before the transfer

- the increases/decreases are recognized as gain/losses

- Thus an asset held for disposal CAN be written up or down in future periods as long as the write-up is never greater than the carrying amount of the asset before the impairment

Loss on Planned Disposition X

Equipment (other asset) X (NRV)

Accumulated Depr X

Equipment X

Involuntary Conversion

Assume a fire destroyed a client’s warehouse:

Write off old warehouse and record $ due from insurance Co.

Due from Insurance 1,200,000

Accum Depre 225,000

Involunt Conversion Gain 405,000

Warehouse 1,000,000

Cash 20,000

Record $ received from Insurance Co. & new Warehouse

Cash 1,200,000

Due from Insurance 1,200,000

Warehouse 1,300,000

Cash 1,300,000

Exchanges with Commercial Substance

- Recognize ALL gain and losses

- Record new asset at FMV. If know #1 below, use it as the debit to the new asset. If #1 is not known use #2:

- FMV given up + cash paid (- cash received)

- FMV of asset received

- Book Value given up + cash paid (- cash received)

Exchanges Lacking Commercial Substance

Assume commercial substances on all exam questions involving non-monetary exchanges unless:

- the fair value of the assets received/relinquished cannot be determined within a reasonable limit

- the exchange is made purely to facilitate the sale of the product to a party that is not a party of the exchange (usually such exchanges take place with a competitor or vendor merely to facilitate future sales to unrelated customers)

- the exchange lacks commercial substance. The question will state that the cash flows are expected to be substantially unchanged as a result of the exchange.

In all three of these exceptions, the carryover basis (book value or carrying amount, adjusted for the cash paid/received as a part of the transaction) is used to measure the transaction instead of the fair value.

- recognize all losses

- defer all gains, unless boot is RECEIVED

- record at lower of:

- FMV given up + cash paid (- cash received)

- FMV of asset received

- Book Value given up + cash paid (- cash received)

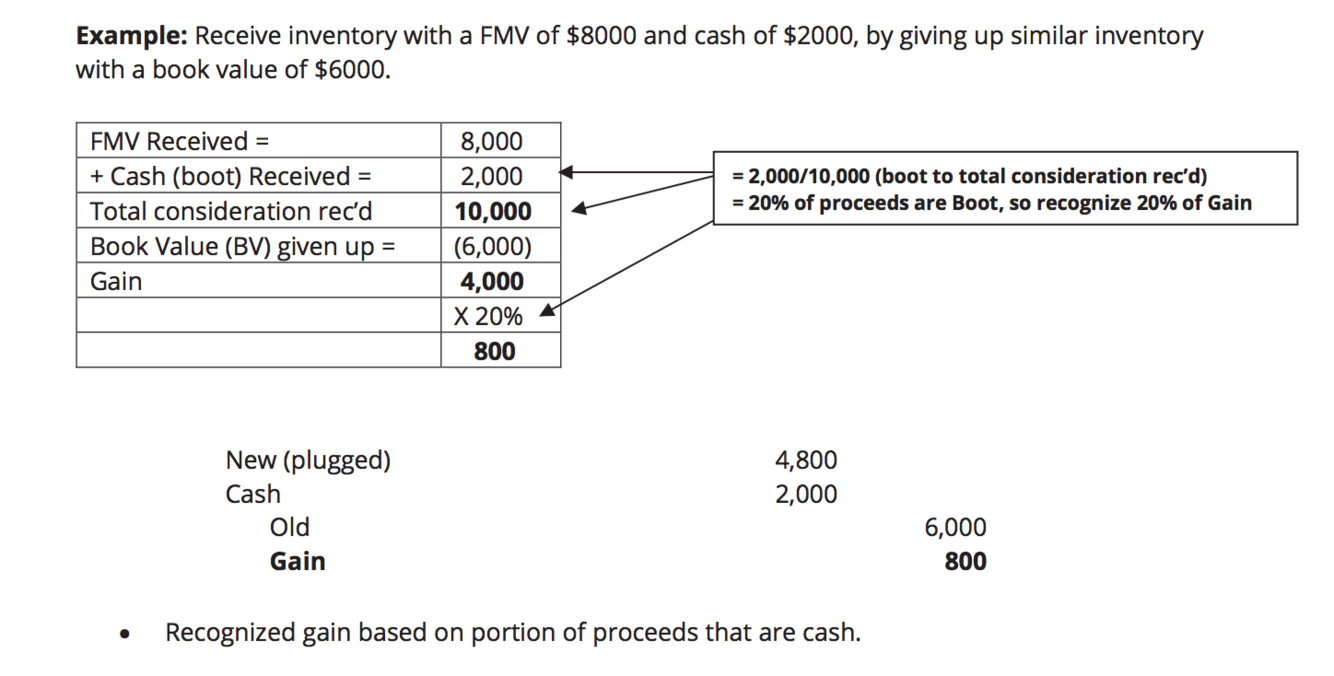

Lacks Commercial Substance - BOOT Received

One type of exchange lacking commercial substance in which gain IS recognized.

- defer all gains unless boot is received, then recognized the gain up to the proprortionate share of boot received to total consideration received. The Ratio to use is: total boot receied/total consideration received (boot + FV of asset received), multipied by the gain

- when the boot recieved is > 25% of the total consideration received (including the boot), the transaction is viewed as a monetary exchange and all of the gain is recognized.