Section A: Estimating Parameters Flashcards

Clark: What are the primary objectives of Clark’s paper? What are the two key elements from those objectives?

Objective 1:

- to provide a tool that describes the loss emergence

Objective 2:

- to provide a way of estimating a range of possible outcomes around the expected reserve

The 2 key elements:

- the expected amount of loss to emerge in some time period

- the distribution of actual emergence around the expected value (stochastic reserving)

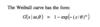

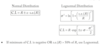

Clark: Expected Loss Emergence

Weibull

- generally provide small tail factor than Loglogistic

- if given Wiebull on the exam, you shouldn’t need to truncate the data or need a tail factor

- Loglogistic you will require to truncate as it has a heavier tail

- note that ‘x’ is cumulative time average so from accident year to valuation point and then half of the last valuation point (so 120 months then ‘x’ is 114)

Clark: Expected Loss Emergence

Loglogistic (Inverse Power)

Clark: What are the advantages of using parameterized curves to determine the expected emergence pattern?

- simple method as we only need to estimate 2 parameters

- can use triangles with partial periods

- indicated pattern is a smooth pattern and will not have random movement seen in the historical age-to-age factors

Clark: What is the benefit of using the Loglogistic and the Weibull curves to derive the reporting pattern?

- Smoothly move from 0% to 100%

- these two models will work when some actual points show decreasing losses; however, if there is real expected negative development then a different model should be used

- e.g. significant salvage recoveries you may see on physical damage

- these two models will work when some actual points show decreasing losses; however, if there is real expected negative development then a different model should be used

- Closely match empirical data

- First and second derivatives are calculable

- Can be used on partial periods

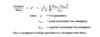

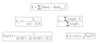

Clark: Estimating Ultimate Losses

LDF Method

µAY;x,y = ULTAY * [G(y|w,ø) - G(x|w,ø)]

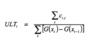

Clark: Estimating Ultimate Losses

Cape Cod Method

Explain why CC is better than LDF method?

µAY;x,y = PremiumAY * ELR * [G(y|w,ø) - G(x|w,ø)]

- Cape Cod method has a smaller parameter variance

- Process variance can be higher or lower than the LDF method

- In general, Cape Cod is preferred to LDF method since:

- LDF method is overparameterized due to less data points as we are using annual triangle

- CC has lower total variance driven by

- reduced number of parameters

- using more information (premium/exposure base)

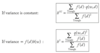

Clark: The distribution of actual loss emergence process variance is given by the following:

σ2 = ?

- assume that c follows an over-dispersed Poisson distribution with scaling factor σ2

- this is the same thing as the Chi-Square error term which is then scaled by n-p

Clark: What are the advantages of using the over-dispersed Poisson distribution?

Advantages

- scaling factors allow us to match the first and second moments of any distribution which offers a high degree of flexibility

- MLE produces the LDF and CC estimates of ultimate losses so can be presented in format familiar to reserving actuaries

Clark: Should we be concerned about estimating ultimate reserves using a discrete (Poisson) distribution?

- the scale factor, σ2, is genearlly small compared to the mean so little precision is lost

- allows for probability mass function (p.m.f.) at zero which mean there can be cases where no change in loss is seen

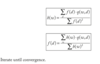

Clark: What is the liklihood estimator of the Poisson distribution?

MLE = Σci * ln(ui) - ui

Clark: What is the formula for the Cape Cod Ulitmate?

ELR = ?

Clark: What is the formula for the LDF ULTi?

Clark: What is an advantage of the maximum loglikelihood function?

- it works in the presence of negative or zero incremental losses

- since its based on expected incremental development and not actual

Clark: What is the total variance of the reserves?

Total Variance = ?

- Total variance is the sum of the process variance and the parameter variance

- Due to the complexity of the parameter variance, it should be given to us on the exam

Process Variance of R = σ2ΣµAY;x,y

Clark: What are the key assumptions of the stochastic reserving model?

1. Incremental losses are independent and iid

In context of reserving:

- independent means one period does not affect surrounding period

- could see positive correlation if all periods are equally impacted by change in loss inflation

- could see negative correlation if large settlement in one period replaces a stream of payments in later periods

- identically distributed assumes the emergence pattern is the same for all accident years (over simplified assumption as mix of business changes would impact this)

2. The variance/mean scale parameter, σ2, is fixed and known

- simplifies the calculations

3. Variance estimates are based on an approximation to the Rao-Cramer lower bound.

- do not know the true parameters so this is an approx.

Clark: Set up the table needed to solve for the reserves.

LDF Method

Clark: Set up the table needed to solve for the reserves.

Cape Cod Method

- MAKE sure to calculate the ELR PRIOR to truncation!

- have to do it this way as per Clark to get the right answer

- parameters will be different since on-level premium is needed so lag factors differ from LDF method

- add a column for OLP

Clark: How do you determine the process variance of the total reserve?

Just multiply the reserve by the scale factor, σ2

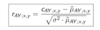

Clark:

rAY;x,y =

What are you looking for when examining the residual plots?

- We want the residuals to be randomly scattered around the zero line

- Can plot the residuals against a number of things to test the model assumptions such as:

- Increment Age (i.e. AY age)

- Expected loss increment - good for testing the variance/mean ratio is constant

- Accident Year

- Calendar Year - to test diagonal effects

Clark: Once the MLE calculations have been completed, there are other uses for the statistics besides the variance of the overall reserve. What are 3 uses?

1. Variance of the Prospective Loss

- Must use Cape Cod for this as we already have the MLE of the ELR

- Can use this to estimate the expected loss if we already have future premium (from budget)

2. Calendar Year Development

- This is AvE as we can estimate the development for the next CY beyond the latest diagonal.

- Good reason for this is that the 12-month development is testable within a short timeframe. One year later we can compare it to actual development and see if its in the forecast range.

3. Variability in the Discounted Reserves

- lower CV as the tail has the greatest process variance but it also gets the deepest discount

Clark: Variance of the Discounted Reserves

Rd = ?

Var(Rd) = ?

Clark: How do you calculate the estimated reserves for partial periods on an AY basis?

- must multiply the Expos(t) by G(x)

- e.g. if its September then the current year will have Expos(t) = 0.75 and G(4.5) and then you would multiply this together to get the adjusted G(x)

- for years not in the first 12 months, the Expos(t) factor is 1

Mack (1994): Mack Chain Ladder Assumption 1

Mack Assumption 1

Expected losses in the next development period are proportional to losses-to-date

E[Ci,k+1 | Ci,1,…,Ci,k] = Ci,k * LDF

- The chain ladder method uses the same LDF for each accident year (volume weighted average)

- Uses most recent losses-to-date to project losses, ignoring losses as of earlier develoment periods

Mack (1994): Mack Chain Ladder Assumption 2

Mack Chain Ladder Assumption 2

Losses are independent between accident years

{Ci,1,…,Ci,I} and {Cj,1,…,Cj,I} between different accident years i≠j are independent.

- a good estimator (fhatk) is unbiased and is as long as we can assume that accident year are independent

E[fhatk]=fk

- cannot make this assumption for triangles impacted by calendar year effects such as changes to claim handling practices or case reserving which affect several accident years similarly

Mack (1994): Mack Chain Ladder Assumption 3

Mack Chain Ladder Assumption 3

Variance of losses in the next development period is proportional to losses-to-date with proportionality constant, ⍺2k, that varies by age.

Var[Ci,k+1 | Ci,1,…Ci,k] = Ci,k * ⍺2k

- stems from the fact that using a volume weighted average has a smaller variance than using a simple average for the LDFs

Mack (1994): Summary of Mack Assumptions

- E[Ci,k+1| Ci,1,…,Ci,k] = Ci,k* LDF

- Losses are independent between accident years

- Var[Ci,k+1 | Ci,1,…Ci,k] = Ci,k * ⍺2k

Mack (1994): What is a major consequence of Assumption 1 where we assume that prior information has no impact on future development?

If Assumption 1 holds, subsequent development factors are uncorrelated because the expected value of fk (the LDF) is not dependent on prior loss development.

Impact: If the book of business typically shows a smaller-than-average increase, Lossk+1 / Lossk < LDFk, after a larger-than-average increase, Lossk / Lossk-1, then the chain ladder method would not be appropriate.

- you would need to make adjustments to the triangle before analysis can be done

Mack (1994): MSE of an accident year’s ultimate loss estimate formula

- remember to take the square root to get the standard error

- s.e.(Rhati) = s.e.(ChatiI)

Mack (1994):

⍺2 = ?

Mack (1994): How do you calculate ⍺2I-1 for the final development period?

Mack (1994): Confidence Interval for the Reserve Estimate

C.I. = ?

- σ is a parameter for lognormal and is not the sd of the reserve - don’t mix these up (same for µ)

Mack (1994): Weights for LDF calculation using different variance assumptions

-

fk0 → assumes that the variance of Cj,k+1 is proportional to 1

- C2ik weighted average of the individual development factors

- violates the third assumption of chain ladder as this assumes variance is proportional to C2ik

- C2ik weighted average of the individual development factors

-

fk1 → assumes the variance of Cj,k+1 is proportional to Cjk

- Cik weighted average of individual development factors

- the usual chain-ladder age-to-age factor fk

- Cik weighted average of individual development factors

-

fk2 → assumes that the variance of Cj,k+1 is proportional to C2jk

- unweighted average or simple average of individual development factors

- proportional to 1 and violates the third assumption of the chain ladder method

- unweighted average or simple average of individual development factors

Mack (1994): Mack Regression Plot

Testing Assumption 1

Mack (1994): Mack Residual Plot

Testing Assumption 3

Mack (1994): Mack Weighted Residual Formulas by Variance Assumption

Mack (1994): Spearman’s test of correlation of adjacent development factors formulas

- Calculate the CI for T

- Reject the null hypothesis that development factors are uncorrelated if T lies outside the CI

Mack (1994): Calendar Year Effects Test Formulas

- First calculate the LDFs

- Convert age to age factors in each column to ranks

- Convert table ranks to S’s, L’s and *’s

- Count the number of S’s and L’s for each diagonal starting top left except ignore the first one as there is only 1 element

- Using formulas, calculate the CI

- Reject the null hypothesis that there are not calendar year effects if Z lies outside the CI

Mack (1994): Mack establishes a CI for the overall reserve. What are 2 things to keep in mind when determing the overall reserve?

- The square of the standard error of R-hat is not the sum of each of the (s.e. (Rhati))2 since each estimator of R-hat is influenced by the same age-to-age factors.

* not independent - you would need a covariance term - To get the CI by accident year, allocate the upper and lower limit of the CI to each accident year in such a way that each accident year has the same confidence level

* e.g. might be that 65% CI for each AY results in 80% CI of overall reserve

Venter: h(w) and f(d) formulas with constant variance

Venter: h(w) and f(d) formulas when using weighted least squares

- on exam could give you picture and you should be able to know what method to use - weighted least-square or basic

Venter: What is the iterative method for Cape Cod?

- Same as the BF method except solving for a single h which is summed over all accident years

Venter: Test of Linearity - Does the following graph pass the linearity test?

How is this test different from the linearity test presented in the Mack (1994) paper?

- No, since there are strings of positive and negative residuals, we can conclude that the age 1 incremental losses are NOT a linear function of the age 0 cumulative losses.

- Mack uses weighted residuals which is different from this test above as these are unweighted. If weighted/normalized, then should see random scattering around zero.

Venter: What test is used for the 5th implication? What are you testing?

Correlation of Development Factors

Calculates the sample correlation coefficients for all pairs of columns in the development triangle, and then counts how many of these are significant to see if correlation exists.